The imputed rental value has been one of the most controversial tax policy issues in Switzerland for decades. While some defend it as a central component of equal tax treatment for tenants and owners, others criticize the regulation as outdated, bureaucratic and distorting. For homeowners with a paid-off mortgage in particular, the taxation of “notional income” often leads to discussions.

What is the imputed rental value?

The imputed rental value is a notional rental value that homeowners have to pay tax on for their owner-occupied residential property.

This is intended to ensure that owners are not in a better tax position than tenants: Those who live in their own property benefit from “saved rent” – and this advantage is taxed as income.

- Basis: cantonal estimates or valuation models

- Amount: usually 60-70% of the market rental value

- Example:

- Market rent: CHF 2 000 / month → CHF 24 000 / year

- Rental value 70% → CHF 16,800 / year taxable income

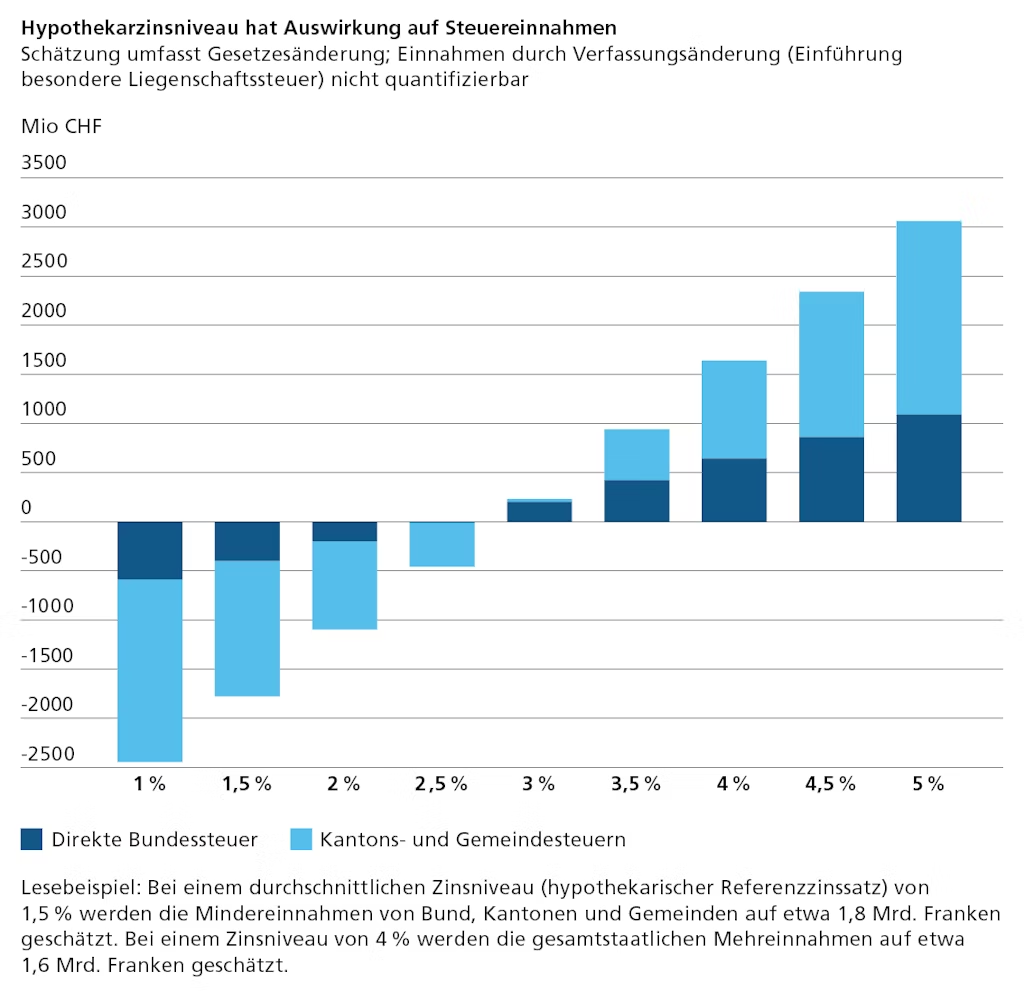

In September 2025, Switzerland decided to abolish the imputed rental value with 57.7% of votes in favor. The results of the vote show how strongly the issue has moved the country.

Deductions and tax effects

In return, owners can claim the following items for tax purposes:

- Mortgage interest

- Property maintenance (flat-rate or actual)

- Building insurance and administrative costs

- Monument preservation costs (if applicable)

For owners with a high mortgage burden in particular, the imputed rental value can be neutralized or even overcompensated for in tax terms. Conversely, a paid-off mortgage often means additional taxable income without deductions.

Current facts and figures

- According to data from the Federal Statistical Office, around 39% of Swiss households own their own home (as of 2023) – and the trend is rising.

- Depending on the canton, the average taxable imputed rental value is between 55 % and 80 % of the effective market value.

- Owners in urban regions are particularly affected, where market rents have risen sharply but the assessment of imputed rental value often lags behind or is regulated differently from canton to canton.

Reform efforts and political discussion

The abolition or reform of the imputed rental value system has been under discussion for years. The following proposals are at the center of this debate:

- Abolition of imputed rental value for owner-occupied residential property

→ but at the same time restrictions on the deduction of debt interest. - Harmonization of the valuation bases

→ more uniform cantonal determination, less unequal treatment. - Introduction of alternative models

→ e.g. flat-rate taxation, replacement by real estate value components.

With the adoption of the bill, the majority of Swiss voters have clearly decided in favor of reform. The actual implementation will be defined in cantonal and federal law over the next few years.

Our assessment from a fiduciary perspective

For many owners – especially those of retirement age – the imputed rental value is increasingly becoming a tax burden, as mortgages are often partially or fully paid off. At the same time, the existing system has clear steering effects: It encourages people to maintain a certain level of debt in order to remain tax-optimized.

From our point of view, three points are central:

🔸 A reform must create planning security and be sustainable in the long term.

🔸 Tax incentives should not lead to excessive debt.

🔸 A fair solution must be coherent across the cantons.

Recommendations for owners

- Check imputed rental value: Depending on the canton, the assessment may be outdated – a request for a review may be worthwhile.

- Exploit deduction options: plan maintenance work or interest payments strategically.

- Long-term tax planning: Have scenarios calculated in good time, especially if you plan to reduce your mortgage in old age.

- Keep an eye on reforms: Any abolition of the imputed rental value would have a direct impact on deductions.

Conclusion

With the acceptance of the vote on September 28, 2025, one thing is certain: the imputed rental value will be gradually abolished in the coming years. This marks the end of decades of political wrangling over one of Switzerland’s most controversial tax instruments. For owners, this means planning in good time to make the most of the future tax framework.